Food

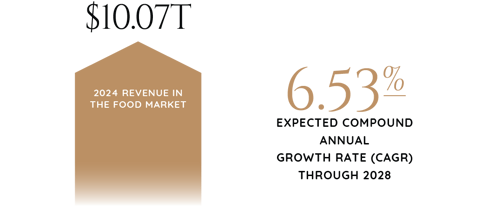

As of 2024, revenue in the food market amounts to $10.07 trillion, with the market expected to grow at a compound annual growth rate (CAGR) of 6.53% annually through 2028. The food market's largest segment is confectionery & snacks, with a market volume of $1.77 trillion. Most of the revenue in the food market is generated in China ($1.63 trillion in 2024).

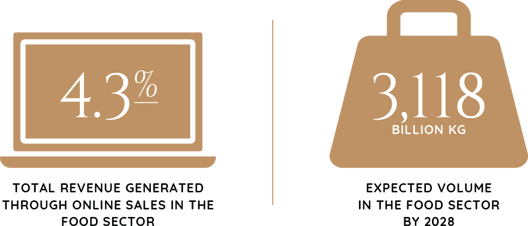

In the food sector, 4.3% of total revenue is generated through online sales, and volume is expected to reach 3,118 billion kilograms by 2028. The food market is expected to grow by 3.9% in 2025.

The food market has to quickly adapt to changing consumer preferences, such as more awareness of "clean label" products, growing consumption of plant-based foods, flexitarian diets, rising demand for regional food, and reducing waste in both the production and the consumption phases. There are also growing trends regarding sustainability, e-commerce, and home delivery.

Retail & Restaurants

The sector has witnessed resilience on behalf of customers combined with a robust labor market, and the trend is expected to continue. 60% of mid-size companies are bullish about the first half 2024, mainly relying on strong consumer spending amidst inflation. Businesses, especially those in the middle market, should adapt to new technological trends to keep up with evolving consumer preferences and mitigate market risks. Retailers can benefit from investing in strategies that sustain growth and protect inventory and profits.

Additionally, scalability can be achieved by collaborating with human workforces and automation. The combination of labor shortages and inflation drives the retail and restaurant sectors to adopt automation, such as self-checkout and artificial intelligence-driven suggestions. Upskilling and data are also used with automation to achieve efficiency and growth.

Supermarkets

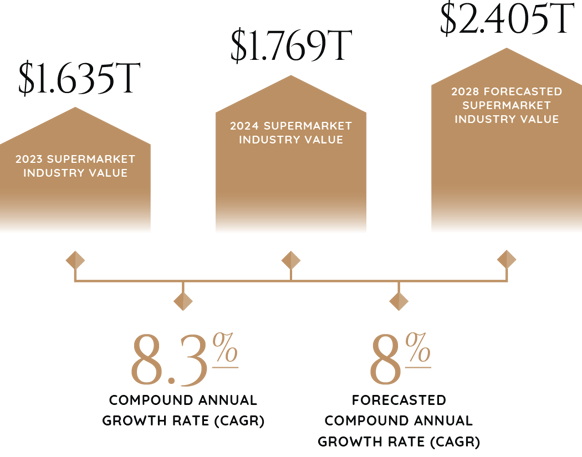

The value of the supermarket industry surged at a compound annual growth rate (CAGR) of 8.3% to grow from $1.635 trillion in 2023 to $1.769 trillion in 2024. This growth can be attributed to shifts in consumer behaviors, growing urbanization, increasing disposable incomes, and more emphasis on convenience and private-label products. Further development forecasts will push the market to reach $2.405 trillion by 2028, staying on pace with a consistent CAGR of 8%.

Factors behind this sustained level of growth include more integration of e-commerce, omnichannel retailing, sustainability initiatives, health and wellness trends, and rising demand for local and organic produce. Other major driving forces in the supermarket include tech advancements such as smart shelves, personalized marketing, loyalty programs, and more contactless and automated solutions.

Social Commerce

According to a 2022 survey, more than 90% of retailers are selling on social media, which has likely only increased in the past two years. Retailers are expected to continue investing in social commerce opportunities, pushing global sales to $1.2 trillion by 2025, which nearly triples levels from 2021. Apparel, electronics, and groceries are expected to drive the social commerce trend forward in the coming years.

The social commerce trend is especially prevalent among younger generations. In recent years, 60% of Gen Z and 56% of millennials reported that they planned to do at least some of their holiday shopping on social media. And in 2022, 63% of shoppers said they bought something via social media.

In the U.S., Facebook and Instagram have been the top social media platforms for retail sales. However, plans to scale back shopping features to focus more on advertising are giving other apps, such as WeChat, the largest social media app in China, the chance to enter the social commerce arena.

More Demand for Same-Day Delivery

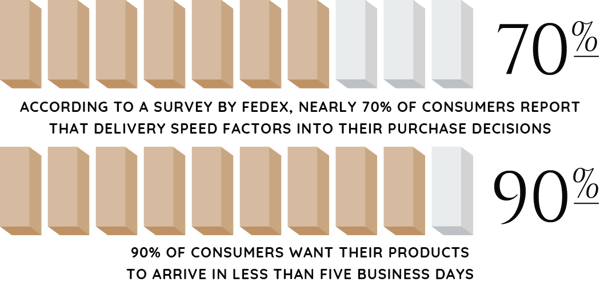

The speed of delivery has become a vital issue for consumers. According to a FedEx survey, nearly 70% of consumers report that delivery speed factors into their purchase decisions. And 90% of consumers want their products to arrive in less than five business days.

Amazon and other large online retailers are seeing rising demand for their same-day delivery programs. More than two-thirds of households in the U.S. subscribe to Amazon Prime, accounting for more than half the population. Also, Prime members spend four times the amount of money non-Prime members spend.

M&A

Retailers will be opting for M&A as a way to better serve specific consumer bases, as several macro trends have changed how and where consumers shop. 2024 is expected to be a record year for M&A in the grocery space. Retailers are looking to maximize returns on their stores, consolidating and creating economies of scale through partnerships and acquisitions.

Consumer migration patterns also factored into retailer M&A deals as consumers moved from urban to suburban and rural areas during the pandemic. This trend has recently started to reverse. Consumers are also changing retail visit habits, hunting for the most value but not the cheapest price. Another trend is how consumers reduce the number of times they visit retail stores, with visits down 2.8% in Q3 2023. Retailers will be enticing customers to visit their stores by offering unique experiences.

There is growing hesitancy among consumer packaged goods companies to make too bold acquisitions. In 2024, companies will look to buy within trendy categories, such as snacking, frozen foods, and healthier options.

Most companies will find it easier this year to focus on growing their portfolios in the current environment, as deal-making is likely to mirror last year. Companies are seeking acquisitions to enter niche categories or geographies. For the last six years, the food and beverage sector has been primarily focused on bolt-on transactions that give companies a more profound presence in certain categories without requiring huge amounts of debt.

Some companies need help to innovate quickly enough, causing them to fall behind, so some are turning to M&A to fill gaps within their portfolios. This is expected to continue to be a significant catalyst for spurring activity in 2024. Health and closer scrutiny of ingredients are likely to be top of mind for consumers in 2024. Cost and value will continue to dominate shopping behavior.

Americas: Sam Smoot at +1 (813) 898 2350 / Smoot@BenchmarkIntl.com

Europe: Michael Lawrie at +44 (0) 161 359 4400 / Lawrie@BenchmarkIntl.com

Africa: Anthony McCardle at +27 21 300 2055 / McCardle@BenchmarkIntl.com

ABOUT BENCHMARK INTERNATIONAL:

Benchmark International is a global M&A firm that provides business owners with creative, value-maximizing solutions for growing and exiting their businesses. Benchmark International has handled over $11 billion in transaction value across various industries from offices across the world. With decades of M&A experience, Benchmark International’s transaction teams have assisted business owners with achieving their objectives and ensuring the continued growth of their businesses. The firm has also been named the Investment Banking Firm of the Year by The M&A Advisor and the Global M&A Network as well as the #1 Sell-side Exclusive M&A Advisor in the World by Pitchbook’s Global League Tables.

Website: http://www.benchmarkintl.com

Blog: http://blog.benchmarkcorporate.com

Share this:

Related