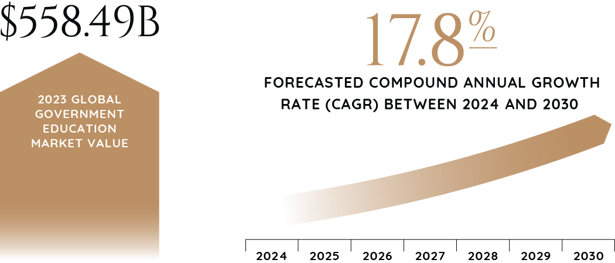

The global government education market was valued at $558.49 billion in 2023 and is forecast to grow at a compound annual growth rate (CAGR) of 17.8% between 2024 and 2030.

Changed admission policies, greater legislative oversight, the expansion of AI, and alternative curricula are among the trends to watch in higher education in 2024. This year, the focus is also returning to fundamentals, such as engagement, retention, well-being, and learner experiences.

Edtech and E-Learning

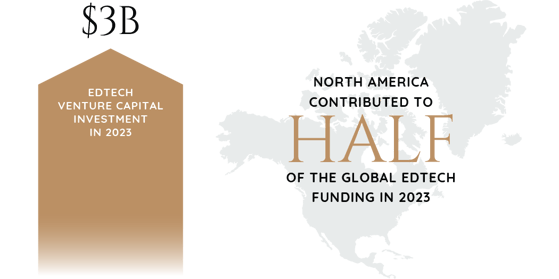

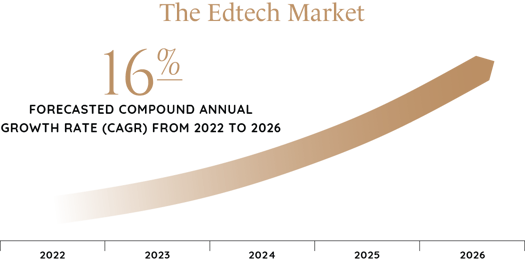

A driving force in the education sector is educational technology, or edtech, which encompasses companies that develop tech solutions to enhance teaching and improve learning. In 2023, billions of dollars were invested in hundreds of tech startup companies worldwide. Edtech venture cap investment reached $3 billion last year, with North America contributing half of the global edtech funding. The edtech market is forecast to grow at a CAGR of 16% from 2022 to 2026.

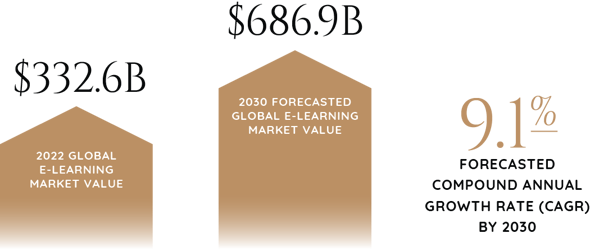

The global e-learning market was worth around $332.6 billion in 2022 and is expected to grow at a CAGR of 9.1% to reach $686.9 billion by 2030. As the demand for e-learning grows, the market is expected to become even more competitive.

Offline Education

While edtech and e-learning are major market drivers, it is essential to note that the offline segment accounted for the largest market revenue share in 2023. This is driven by government investments in traditional educational infrastructure, teacher training for conventional classroom settings, and the significance of physical learning environments. Also, the offline space focuses on in-person interaction between students and teachers, which promotes a more collaborative and social learning environment.

Key Trends in Government

The public sector continues to evolve, focusing on integrating technology, supply chain resilience, and adopting sustainable practices. Key areas for 2024 include digital transformation and AI, strategic investment in infrastructure, sustainability and resilience, and cybersecurity and ethical AI challenges. AI is changing the skills needed by government employees, specifically in call centers.

Other trends to note are that:

- Tax and revenue agencies are using emerging technologies for compliance

- More governments are recognizing the risk posed by legacy technologies for policy implementation

- Governments will create three segregated regional tech markets to pursue digital sovereignty: the European Union, Sino-Russian, and U.S.-led Indo-Pacific. The rise of these markets will force public and private sector organizations to adjust their supply chains and the global tech industrial complex to choose who they want to serve and from where

By Region

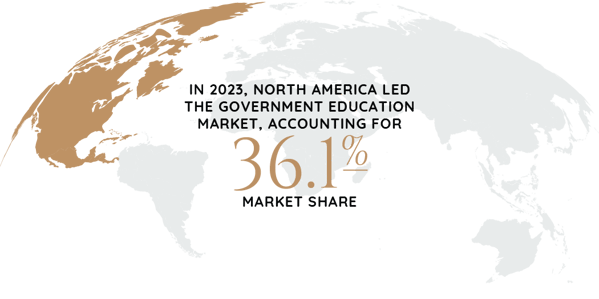

Last year, North America led the market, accounting for 36.1% of the market share. Significant revenue generation in this region is due to well-established and financially robust education systems, including primary, secondary, and higher education institutions. There is also a high level of government investment in education, advanced tech infrastructure, and a strong emphasis on research and development. This boosts North America's overall competitiveness when it comes to educational institutions. Additionally, the region's dominance in the industry can be attributed to prominent global universities and a wide range of academic programs.

The Asia-Pacific region is poised to see significant growth in the market in 2024, as it is home to a large and rapidly growing population with a large proportion of young students. Increasing demand for education, especially at primary and secondary levels, is driving market growth, and many countries in the region are investing in education infrastructure and policies that enhance the quality and accessibility of education.

M&A

A high level of M&A activity by leading players characterizes the market for government education. Large educational corporations and tech companies often engage in M&A to strengthen their market position, grow their service offerings, and improve their capabilities to deliver educational solutions.

Nearly 300 listed education companies hold a combined market cap of around $200 billion at any time, with significant fluctuations over the past few years. Small defense and government tech companies need an M&A strategy, especially with many larger buyers currently pausing on M&A deals. M&A is a key strategy for minor defense and government tech companies seeking organic growth opportunities, such as winning prime contracts in competition against established industry players.

Industry-focused PE firms that are equipped to provide upfront capital offer proven M&A capabilities. They can spot acquisition targets and help companies execute strategies effectively, significantly reducing the risks associated with a solo growth approach.

Americas: Sam Smoot at +1 (813) 898 2350 / Smoot@BenchmarkIntl.com

Europe: Michael Lawrie at +44 (0) 161 359 4400 / Lawrie@BenchmarkIntl.com

Africa: Anthony McCardle at +27 21 300 2055 / McCardle@BenchmarkIntl.com

ABOUT BENCHMARK INTERNATIONAL:

Benchmark International is a global M&A firm that provides business owners with creative, value-maximizing solutions for growing and exiting their businesses. Benchmark International has handled over $11 billion in transaction value across various industries from offices across the world. With decades of M&A experience, Benchmark International’s transaction teams have assisted business owners with achieving their objectives and ensuring the continued growth of their businesses. The firm has also been named the Investment Banking Firm of the Year by The M&A Advisor and the Global M&A Network as well as the #1 Sell-side Exclusive M&A Advisor in the World by Pitchbook’s Global League Tables.

Website: http://www.benchmarkintl.com

Blog: http://blog.benchmarkcorporate.com

Share this:

Related